Capital in Malaysia #3: Investments and Profits, Do They Matter Under Malaysia’s Political Capitalism?

A bit of exposition on profits and investment before diving into looking at the sectors that conglomerate capital thrive in.

After having laid out my rough sketch of political capitalism in Malaysia, a natural subject to unpack next is one from the first premise — the rate of return and the nature of profits. The often-discussed subject of reviving Malaysia’s GDP growth cannot be divorced from how profits are made in the recent domestic and global economic environment. Attempts to return to the ‘promised land’ of 8-9% GDP growth — seen right before the 1997-8 Asian Financial Crisis (AFC) — and the tired invocation of the middle-income trap frame much of this discussion. Profits — or in more Marxian terms, surplus value — especially at a national level in aggregate, are conditioned by factors like the rate of investment, the way rents and industrial policy is deployed and how much labour can be exploited.

Investments and Economic Growth

The endless talk by politicians, government officials and capitalists in the Malaysian press about FDI (foreign direct investment) is gesturing towards a specific and fundamental belief that investment drives economic growth. Tim Barker, in his response to Brenner and Riley’s Seven Theses, outlines Brenner’s link between profits, investment and economic growth:

“First: why do profits matter? According to Brenner, they matter because investment matters: ‘The profit rate is the key to the economy’s health because it is the key to the growth of investment.’ Investment matters for two reasons: because investment demand is the most important element of aggregate demand, which in turn determines overall employment and output; and because investment leads to productivity increases and therefore to an increase in potential output. In his words: “Leaving aside the government, I see the growth of demand in the private sector as basically resulting from the growth of investment, dependent upon the profit rate. The growth of investment creates both the growth of employment and, by way of the growth of employment and the growth of productivity, the growth of real wages. So, the growth of investment creates the growth of demand both for capital goods—plant and equipment—and for consumer goods.” In what way are profits the key to investment? Brenner cites two mechanisms. First, retained earnings are an important source of financing for investment: ‘Higher profit rates make for higher available surpluses.’ Second, profit signals provide the motive for new investment: ‘companies have little choice but to regard the realized rate of profit as the best available indicator of the investment climate, the expected rate of profit.” — (page 45-46)

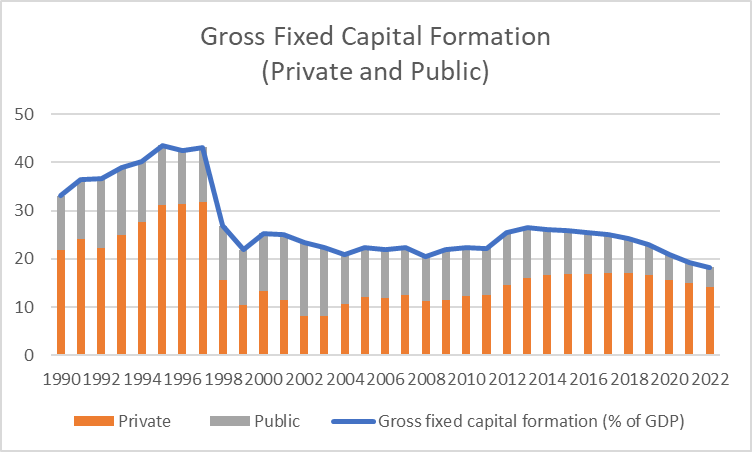

The two mechanisms Brenner posits are central to understanding the nature of economic growth in the Malaysian context. Investment in mainstream economics is measured through gross fixed capital formation (GFCF), defined as “the acquisition of produced assets (including purchases of second-hand assets), including the production of such assets by producers for their own use, minus disposals”. It includes “land improvements (fences, ditches, drains, and so on); plant, machinery, and equipment purchases; and the construction of roads, railways, and the like, including schools, offices, hospitals, private residential dwellings, and commercial and industrial buildings.”

Based on the graphs below, Malaysia’s GDP growth has not always closely tracked the levels of investment. However, the years that see the most significant levels of growth have been 1987-1997, years where the GFCF as a percentage of GDP has been relatively high. The role of the private sector is not insignificant in this matter. The collapse in private investment during the Asian Financial Crisis has not seen a recovery. The brief bump from 2010 to 2018 coincides with the Najib-era rise of GLCs as major players in the economy in which the lines between public and private were blurred.

Given the outsized attention it gets in the press, one might think the role of foreign direct investment (FDI) is the most important driver of economic growth. Yet, during the 90s, it would only reach heights of 8.8% and average 5.8%. Furthermore, much of the FDI coming in did not directly contribute to GFCF as it can also take the form of brownfield investments — purchase of existing capital stock or equity. So, under conditions where private investment is weak — a tentative sign of poor profitability in the market, any boost to profitability can make all the difference.

Economic Policy and Profitability

In any capitalist country, the state — and the political class that controls it — has at its disposal the means to enhance profits to whatever ends it chooses. The rough categories of these tools can be mapped onto the factors of production — land, labour and capital. In the heyday of industrial policy under Mahathir in the 1980s, the Malaysian state subsidised production in various forms: the use of Special Economic Zones, land grants, exemptions or accelerated access to foreign labour, government grants, and cheaper or easier access to financing. While these initiatives constitute more active measures, the policy-based, passive or possibly ‘indirect’ means of boosting profitability would take various other forms.

The long history of labour suppression and the “tacit go-ahead” to allow illegal immigration from Indonesia, Thailand and the Philippines (see Jomo & Todd, 1994, p. 149-50) by the Malaysian state brings down to cost of labour for extractive, manufacturing and low-productivity service sectors. The awarding of government contracts to selected firms — overvalued or not — is an indirect capital injection into said firms that could help them roll capital into other ventures. The unspoken or unseen favour of the Malaysian state or its political class towards a particular company can open the doors to bank loans that would otherwise be closed to ordinary firms. Jomo and Khan go into six types of rents that states can deploy for whatever purposes they see fit (see appendix below), many of which the Malaysian state and political elite have employed over their decades of rule.

Considering Conglomerate Capital

These direct and indirect means of increasing firm profits have tended to advantage larger companies or corporations over their small and medium counterparts. As goes one of the central premises of monopoly capital theory, size translates to political and economic access, and in the cases that we will look at later in this series, vice versa as well. Under conditions of stagnant growth and a poor investment climate, conglomerates — private, public or hybrid —represent key players in the Malaysian economy. An estimate by a mainstream economist posits the large economic footprint of GLCs and GLICs with their assets totalling 51% of GDP, their debt more than 15% and their revenue approximately 25%. Coupled with private conglomerates, these figures would increase by a considerable amount.

The rise of conglomerates most definitely preceded the AFC but their role in the economy would become crucial after as potentially more stable conduits for capital recirculation and investment — albeit in low-tech low-productivity sectors. Returning to Brenner and Riley, the idea that assistance to these politically connected conglomerates constitutes “politically engineered upward redistribution” is not far-fetched as the state would use tax revenue for these measures. However, more indirect and unseen measures merit greater attention as they silently shape the domestic investment climate and conditions of profitability.

The next entry in this series will aim to demarcate the boundaries and overlaps between conglomerate capital, crony capital and state capital. The one to follow that would be defining the ‘safe sectors’ along the lines described by Khoo Boo Teik in the previous entry, looking specifically at how the state generates and maintains the profitability of these sectors, and what about these sectors potentially make it easier for the state to step in.

APPENDIX

Table 1.1 Rents and the rights sustaining them (page 65, Jomo & Khan)

Table 1.2 Commonly identified but misleading 'differences between rents (page 67, Jomo & Khan)

Table 1.3 Relevant growth and efficiency implication of different rents (page 69, Jomo & Khan)